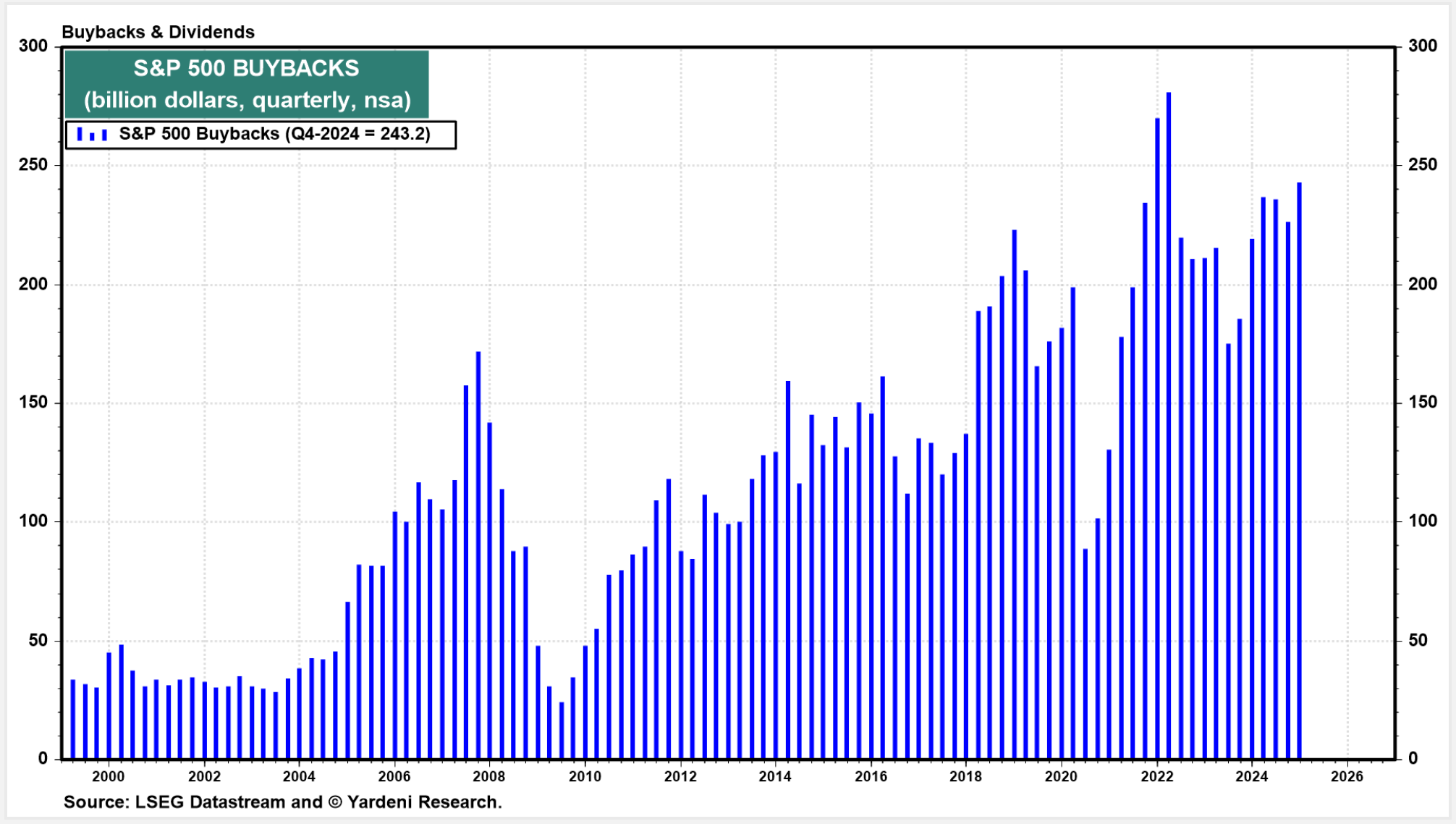

Stock Buybacks: An Effective or Misunderstood Tool?

Understanding the Role of Stock Buybacks in Capital Allocation and Shareholder Value Creation

Introduction

Stock buybacks are a commonly used strategy by publicly traded companies to return capital to their shareholders. This process occurs when a company uses its available cash to purchase its own shares in the open market or through a direct offer. The result is a reduction in the total number of outstanding shares, which increases earnings per share (EPS) if the company's earnings remain constant.

However, stock buybacks are often subject to controversy and criticism, some of which is more political than economic. This article delves into what stock buybacks are, the criticisms they receive, their differences from dividend payments, and their actual impact on shareholder value creation.

Common Criticisms of Stock Buybacks

Many arguments against stock buybacks stem from ideological debates about private ownership of capital and often focus on a false dilemma of "capital versus labor." The most common criticisms include:

Buybacks versus Wages and Bonuses: It is frequently argued that buybacks suppress employee wages and benefits. However, this reasoning overlooks that buybacks are funded with cash generated from the company’s profits, not from funds allocated to employee compensation.

Impact on Economic Growth and Productivity: Some critics blame buybacks for slow economic growth, low productivity, and stagnant wages. However, these claims are mainly political arguments. In fact, buybacks often benefit employees through stock option plans or incentives that align their interests with those of the company.

Misconception About Impact on Investment: Stock buybacks do not prevent companies from making new investments. On the contrary, a company with higher earnings per share has greater purchasing power and better access to financing on favorable terms.

Apple Inc. has been one of the most prominent users of stock buybacks, spending over $400 billion on repurchases since 2012. Despite these massive buybacks, Apple has continued to invest heavily in R&D and expand its product ecosystem.

Strategic Options for Profit Allocation

Profitable companies have multiple alternatives for allocating their capital, often using a mixed approach that combines several strategies:

Reinvesting in the Company: Funding new products, markets, or business initiatives to promote long-term growth.

Debt Reduction: Paying down existing debt using profits or through balance sheet transactions.

Mergers and Acquisitions (M&A): Acquiring competitors, achieving economies of scale, or capturing cost synergies.

Cash Retention: Reserving funds to face potential financial difficulties in the future.

Stock Buybacks: Reducing the number of outstanding shares to increase EPS, or financing incentive programs for employees and executives.

Dividend Payments: Distributing profits directly to shareholders in the form of dividends.

Berkshire Hathaway, under Warren Buffett, has increasingly utilized stock buybacks in recent years, especially when shares are trading below intrinsic value. Buffett’s philosophy is that repurchases should be opportunistic and driven by valuation.

Stock Buybacks vs. Dividends: Tax Differences

From a tax perspective, stock buybacks and dividends have distinct implications that affect shareholder profitability:

Taxes on Dividends: Dividends are considered ordinary income and are taxed in the year they are received. Depending on the jurisdiction, they are often subject to higher taxes than capital gains. In the U.S., while qualified dividends have preferential rates, they are generally higher than long-term capital gains rates.

Taxes on Stock Buybacks: Shareholders who sell shares during a buyback only pay taxes on the realized capital gains, i.e., the difference between the sale price and the original cost basis. Moreover, long-term capital gains often benefit from lower tax rates. Those who do not sell their shares during a buyback face no tax burden at all.

“When companies make repurchases, they’re doing it because they think their stock is cheap. And the only way you can do that is by giving shareholders a benefit at that moment.” — Warren Buffett

Are Stock Buybacks Harmful?

Stock buybacks should not be considered an expense that competes with wages, research and development, or any other productive use of capital. In reality, they are an efficient capital allocation tool that can benefit shareholders when used strategically.

Moreover, the flexibility offered by buybacks makes them an appealing mechanism for returning capital over the long term, especially when shares are undervalued and repurchasing them generates significant value for remaining shareholders.

General Electric (GE) executed massive buybacks during the early 2000s at inflated prices, which subsequently weakened the company’s balance sheet during the 2008 financial crisis.

Conclusion

Far from being a threat to the economy or a barrier to growth, stock buybacks are a legitimate and efficient method of returning capital to shareholders. The key lies in their proper implementation. Investors must analyze each case individually to determine whether buybacks genuinely contribute to sustainable growth and the company's profitability.

Source

The Case for Dividend Growth: Investing in a Post-Crisis World by David Bahnsen.